4 min read

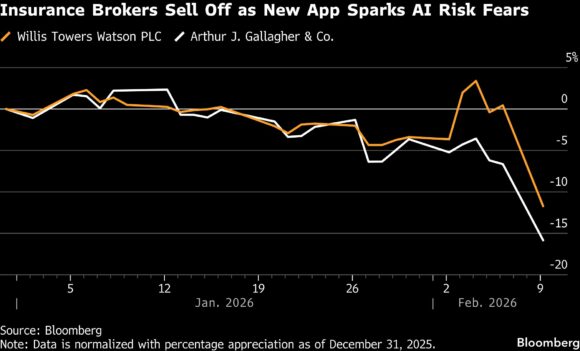

In February 2026, the launch of insurance comparison and quoting applications inside generative AI platforms has sent a clear signal to financial markets: distribution models are under review. When insurance apps became available within conversational AI tools such as ChatGPT and Claude, investors reacted quickly. Share prices of major global brokers, including Willis Towers Watson and Aon PLC, fell, alongside UK price-comparison brands such as GoCompare and MoneySuperMarket.

For professionals working in regulated businesses, this market response raises deeper questions. Is AI genuinely threatening traditional intermediation, or is this another cycle of overreaction driven by technology headlines? This article explores the background to the sell-off, the argument that AI represents a disruptive force, and the counterargument that the fundamentals of insurance distribution remain resilient.

How AI Triggered a Market Reaction

The immediate catalyst was the release of insurance comparison and quotation tools integrated directly into large language model platforms. These tools allow consumers to request motor or home insurance quotes through a conversational interface, without visiting traditional broker websites or price-comparison platforms. This development was widely reported in financial media, including Reuters and Insurance Journal, which noted that US and European insurance stocks experienced their sharpest one-day declines in months following the announcement.

In the UK, where price comparison websites are deeply embedded in consumer behaviour, the reaction was equally visible. Analysts interpreted the news as a potential threat to two pillars of insurance distribution: broker advisory services and digital comparison platforms. The logic was straightforward. If AI can aggregate offers, explain policy features, and personalise results in real time, it could become the first touchpoint for millions of consumers.

This fear was amplified by the scale of AI adoption. Unlike earlier insurtech start-ups, generative AI platforms already have vast user bases. Investors, therefore, saw the possibility of rapid behavioural change rather than slow market entry. The result was a sell-off driven more by narrative than by the immediate impact on earnings, a phenomenon common in technology-led market shifts.

AI Signals a Structural Shift in Distribution

Supporters of the market’s reaction argue that AI-driven insurance tools mark a genuine inflexion point in how customers access financial products. Distribution has always been vulnerable to technology. Comparison websites disrupted high-street brokers; now AI threatens to disrupt comparison sites themselves.

Consulting firms have reinforced this view. McKinsey has argued in recent digital transformation research that customer journeys in financial services are moving away from websites and apps towards conversational interfaces and embedded ecosystems. According to McKinsey, firms that fail to adapt their distribution strategies risk losing direct relationships with customers to technology platforms that control the interface.

Similarly, Deloitte has highlighted that generative AI can compress the buying journey by combining research, comparison and recommendation into a single interaction. For insurance, this could mean fewer clicks, fewer intermediaries, and greater price transparency. From an investor’s perspective, this creates uncertainty over future margins and customer acquisition costs, justifying a repricing of listed brokers and comparison firms.

There is also a strategic concern for regulated businesses. If AI platforms become dominant gateways, insurers and brokers may become dependent on external technology providers for distribution. This mirrors what happened in travel and retail, where aggregators and platforms captured much of the customer value. In that context, the recent stock market dip can be seen not as panic but as a rational reassessment of long-term competitive dynamics.

The Reaction Overstates AI’s Immediate Impact

However, many industry leaders and analysts argue that the market has overstated the disruptive power of current AI insurance tools. While AI can summarise products and generate indicative quotes, it cannot yet replace the regulatory framework that governs insurance advice and sales in the UK.

As reported by The Times and other business publications, executives from UK comparison sites have stressed that generative AI models are not designed to provide consistent, auditable advice. The Financial Conduct Authority (FCA) rules require transparency, suitability assessments, and clear accountability. A conversational AI output, generated probabilistically, struggles to meet these standards without significant governance layers.

Furthermore, the core business of large brokers is not simple retail insurance. Firms like Willis Towers Watson and Aon focus heavily on commercial risk, reinsurance, and complex advisory services. These activities rely on negotiation, bespoke analysis, and long-term relationships with underwriters and corporate clients. AI may assist these processes, but it is unlikely to displace them in the short or medium term.

UK price comparison platforms also retain structural advantages. They have established insurer partnerships, consumer trust, and compliance frameworks built over decades. Rather than being displaced, they are already experimenting with embedding AI into their own services to improve customer experience. In this sense, AI may become a tool for incumbents rather than a weapon against them.

Market history suggests caution. Similar fears emerged with robo-advisers in wealth management and with blockchain in payments. In both cases, incumbents adapted, integrated the technology, and maintained their relevance. The same pattern may play out in insurance.

Conclusion

The recent dip in insurance broker and price comparison stocks reflects more than just earnings concerns. It captures a broader anxiety about who will own the customer relationship in an AI-driven economy. For regulated businesses, this moment should be seen as a strategic warning rather than a verdict.

AI has the potential to reshape how consumers research and purchase insurance, and investors are right to factor this into valuations. Yet the regulatory complexity of insurance, combined with the depth of expertise required for many products, suggests that intermediaries still play a vital role.

The most likely outcome is not replacement but evolution. Brokers and comparison platforms that integrate AI responsibly, while preserving compliance and trust, will remain central to the ecosystem. Those who ignore the shift may face a longer-term decline.

For professionals in regulated sectors, the lesson is clear. Market sentiment can move faster than structural change, but it often points to where strategy must evolve. The recent stock market reaction is less about panic and more about a reminder that distribution, data, and customer interfaces are becoming the new battleground in insurance.